1-855-410-7971

1-855-410-7971

You’ve likely heard of wills and trusts, but do you truly understand the difference between the two? In this article, we’ll discuss key terms, highlight the differences, and explore various aspects of both options to help you make the right decision.

What is Will?

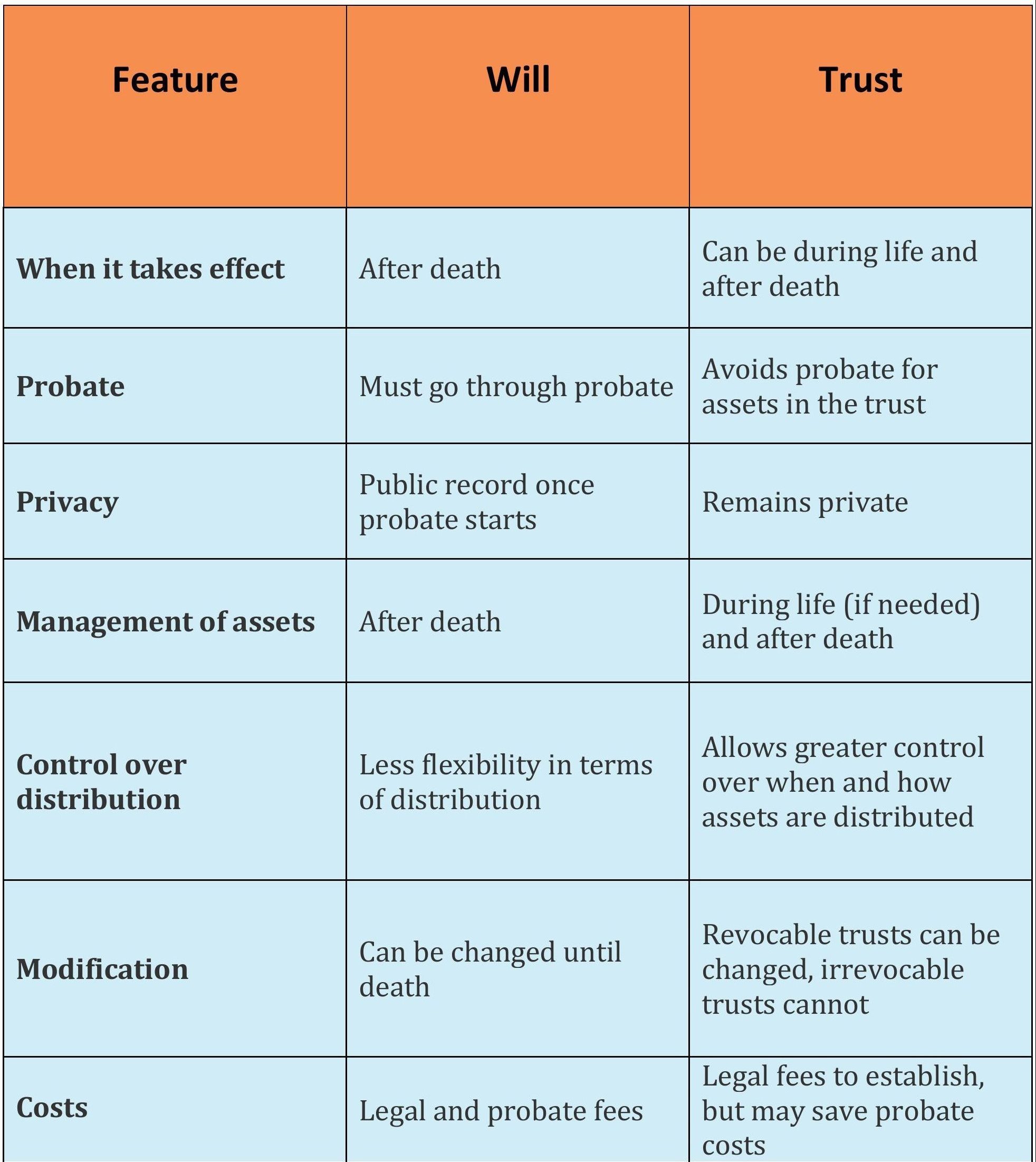

A will is a legal document that outlines how you want your assets (like money, property, or belongings) to be distributed after you pass away. It also allows you to name an executor, who will be responsible for carrying out your instructions. A will only take effect upon your death, and it often goes through a legal process called probate, where a court oversees the distribution of your estate to make sure everything is done correctly.

Key Points That You Should Know About:

- Executor: The individual assigns an executor in the will, who is responsible for ensuring that the terms are carried out.

- Beneficiary: Individuals or organizations named in the will to receive the deceased’s assets. These can include family members, friends, or charitable organizations.

- Guardian: If the deceased has minor children, a guardian may be appointed in the will to care for them.

- Distribution of Assets: Will specify who will inherit assets and name a guardian if minor children are involved.

- Does not avoid probate costs: Probate fees can reduce the value of the estate left to beneficiaries.

- Residuary Estate: The remainder of an estate after all debts, taxes, and specific bequests have been paid.

- Intestate: If someone dies without a valid will, they are considered to have died “intestate.” This means that provincial laws will determine how the estate is distributed.

What Are The Rules of Intestacy?

These are the General Rules for Intestate Succession;

1. If the deceased has a spouse but no children:

- The entire estate goes to the surviving spouse.

2. If the deceased has a spouse and children:

- The spouse receives a preferential share, which varies by province.

- The remainder is divided between the spouse and children, with the exact split depending on provincial laws.

3. If the deceased has children but no spouse:

- The estate is divided equally among the children.

4. If the deceased has no spouse or children:

- The estate goes to the parents of the deceased.

- If no parents are alive, the estate is divided among siblings.

5. If there are no surviving immediate family members:

- The estate may go to nieces, nephews, or cousins, following a set order of relatives.

6. If no relatives are found:

- The estate escheats to the Crown, meaning the government takes control of the assets.

Each province has slight variations in these rules, but the overall structure is similar across the country.

What is Trust?

A trust is a legal arrangement where you (the grantor) transfer ownership of your assets to a trustee, who manages those assets on behalf of your beneficiaries. A trust can take effect while you are still alive (called a living trust) or after your death (a testamentary trust). Trusts give you more control over how and when your assets are distributed, and they usually avoid probate, meaning the process is private and often quicker.

Important Aspects to Know:

- Revocable Trust: A trust that can be altered or revoked by the settlor during their lifetime. It allows for flexible management of assets but does not protect them from creditors or estate taxes. In a revocable trust, the settlor can also serve as a trustee while alive.

- Irrevocable Trust: A trust that cannot be altered once it is established. The assets placed in an irrevocable trust are typically protected from creditors and taxes but are no longer under the direct control of the settlor.

- Trust Corpus (Principal): The assets that are placed into the trust, such as real estate, investments, or cash. The trustee manages these assets according to the terms of the trust.

- Trust Deed: The legal document that outlines the terms, conditions, and rules governing the trust. This document establishes the trustee’s duties and the rights of the beneficiaries.

- Distribution: The way the trust assets are passed to the beneficiaries, which can be immediate or scheduled over time depending on the terms of the trust.

- Spendthrift Clause: A provision that protects the trust assets from being squandered by the beneficiary or claimed by the beneficiary’s creditors. This ensures that the assets are preserved for the long-term benefit of the beneficiaries.

Key Differences at a Glance:

Which Option Is Best for Your Loved One?

The key thing to keep in mind is that both wills and trusts can provide different benefits. Therefore, ruling out one as better than the other might not be the best approach. Deciding which option to choose will depend on your needs, goals, and assets.

These factors can help you decide;

- If privacy is a concern – Trusts are a better option as they remain private, unlike wills, which become public after death.

- If avoiding probate is a priority – Trusts are more effective since assets in a trust bypass probate.

- For simpler estates – Wills are generally sufficient for estates without complex asset distribution needs.

- Ongoing care needs – Trusts offer more control and can be designed to manage assets during a person’s lifetime, ideal for individuals who need ongoing financial management due to illness or incapacity.

Read More: Talking to Your Elderly Parents About Financial Planning

Can You Have Both a Will and a Living Trust?

You can have both a will and a living trust as part of a comprehensive estate plan. While these processes serve different purposes, they can work together to ensure that your assets are managed and distributed according to your wishes.

How Wills and Trusts Work Together?

Here’s how they complement each other:

Catch-All Function: The Pour-Over Will Even if you have a living trust, some assets might not be included in it. This is where a pour-over will come in. A pour-over will ensure that any assets not already transferred into the trust during your lifetime will be moved into the trust after your death. This guarantees that all your assets are ultimately distributed according to the trust’s terms.

Addressing Personal and Family Matters A will can appoint guardians for minor children or dependent adults, which a living trust cannot do. It also allows for the distribution of personal items like heirlooms, jewelry, or sentimental belongings, which may not be included in a trust.

Avoiding Probate A living trust helps you avoid probate for assets held in the trust, saving time and reducing costs. However, any assets not transferred into the trust (either deliberately or by oversight) will be subject to probate if only a will is in place. The combination of a will and a trust ensures that all assets are covered, even if they require probate.

Benefits of Having Both a Will and a Living Trust:

- The trust handles large assets, while the will covers assets not in the trust and appoints guardians.

- The trust allows control over how and when assets are distributed, and the will handles personal wishes like guardianship.

- A living trust provides quick access to funds, while a will requires probate, which may delay access.

Want To Learn More?

Looking for professional care? Reach out to us at wecare@considracare.com and we will be happy to assist you with the care needs of a loved one.

Final Thoughts:

Whether your loved one should choose a will, a trust, or both depends on their unique financial and personal circumstances. Family members play an essential role in ensuring that the estate planning process is aligned with the elder’s needs and wishes. Both wills and trusts offer valuable tools for managing and protecting assets, but understanding the distinctions between them is key to making informed decisions.

FAQ’s

1. Can a trustee be a beneficiary?

Yes, a trustee can also be a beneficiary of the trust. However, they must act in the best interest of all beneficiaries and manage the trust impartially. The trustee has a fiduciary duty to follow the terms of the trust and ensure that all beneficiaries are treated fairly.

2. How does a family trust work in Canada?

A family trust in Canada is a legal arrangement where assets are transferred to a trustee, who manages them on behalf of family members (the beneficiaries). Family trusts are often used to protect assets, manage wealth across generations, and optimize tax planning. The trust can provide income to beneficiaries while keeping control over how and when assets are distributed.

3. At what net worth do I need a trust?

There is no specific net worth that dictates the need for a trust. Trusts are useful if you have significant assets (such as real estate or investments), complex family situations, or specific goals, like protecting assets from probate, ensuring long-term financial management, or providing for minor children or dependents. Trusts can be beneficial for estate planning regardless of the exact value of your estate.

4. Who inherits if a beneficiary dies in Canada?

If a beneficiary dies before the estate is distributed and there is no alternate beneficiary named, the beneficiary’s share typically passes to their heirs under their own will or intestacy laws. However, if the will or trust includes provisions for what happens in this scenario (such as naming a contingent beneficiary), those instructions will be followed.

5. Is a living trust more expensive than a will?

Yes, setting up a living trust is typically more expensive than drafting a will due to its complexity. However, the trust can save money in the long run by avoiding probate costs.

6. What assets should go into a trust?

You can place many assets into a living trust, such as real estate, bank accounts, investments, and business interests. However, some assets like retirement accounts and life insurance policies should not be transferred into a trust directly but can name the trust as a beneficiary.

7. Can a living trust replace a will?

No. A living trust cannot replace a will entirely because it does not allow you to name guardians for minors or dependents, nor does it typically handle personal items. A will is necessary for these specific matters.

Fakiha is an experienced writer at ConsidraCare with an optimistic interest in life. She has a proactive approach to improving health and wellness for seniors. She offers well-researched and thoughtful information to help individuals make informed healthcare decisions for themselves and their loved ones.